Project

AI Portfolio Advisory System

Foundation-model risk profiling and objective-aware portfolio optimization for personalized investing.

Python TabPFN PyTorch Streamlit Deep Q-Networks Portfolio optimization Market regime detection

Business context

Most robo-advisors rely on static questionnaires and a small set of fixed portfolio templates. This project explored a more adaptive alternative: using tabular foundation models for risk profiling and objective-aware reinforcement learning for portfolio construction.

Outcome

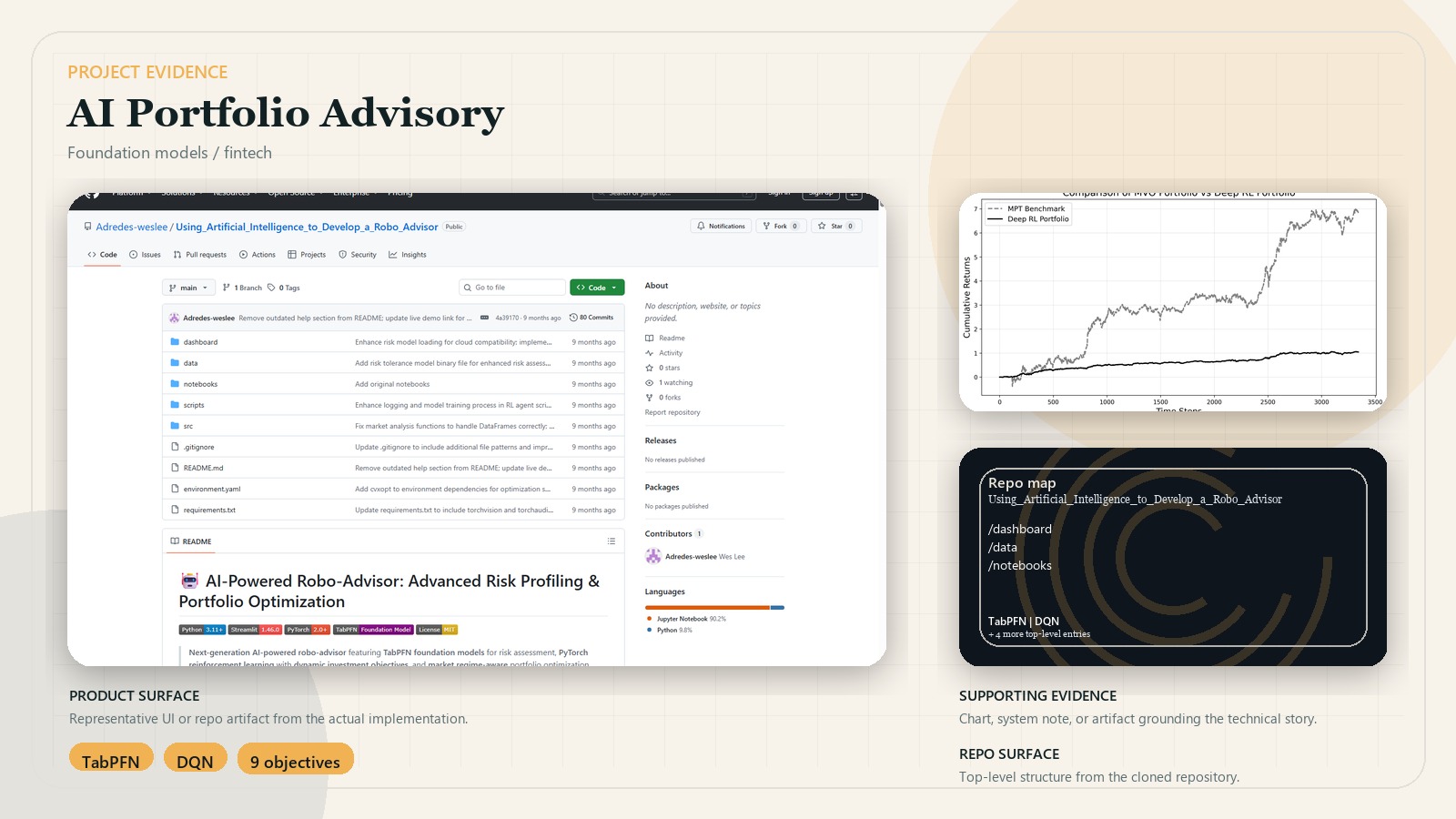

- Combined TabPFN-based risk profiling with PyTorch DQN portfolio optimization.

- Supports multiple investment objectives and market-regime-aware behavior instead of one fixed recommendation path.

- The local TabPFN workflow reports risk-prediction accuracy above 0.85 R^2 in the documented setup.

- Ships a Streamlit dashboard that keeps the system usable in both local and cloud-constrained environments.

Key decisions

- Used TabPFN for risk assessment instead of only traditional tabular ML.

- Trained objective-specific agents instead of one universal portfolio policy.

- Added market-regime awareness so recommendations respond to changing conditions.

- Designed separate local and cloud execution paths so the product remains usable when full RL inference is not feasible.

System design

User inputs feed a risk-profiling layer, then route into objective-aware portfolio logic that selects or simulates the appropriate optimization path. The application adapts between full local-AI mode and lighter cloud-compatible behavior while preserving the same overall user journey.

Stack

- Python, TabPFN, PyTorch, and portfolio optimization utilities

- Streamlit for the advisory product surface

- Risk profiling, regime detection, and objective-aware RL components